Managers of law departments (and of law firms) often believe that there is an identifiable connection between one set of numbers and another. Perhaps they sense that the size of the plaintiff’s law firm has some bearing on the cost of defending a lawsuit; they feel the number of patents applied for rises and falls with their company’s R&D investment; or they’ve noticed that client satisfaction scores relate to keeping close to budget. Fortunately, those types of subjective impressions of managers can be tested and quantified.

Correlation is the statistical tool to quantify such possible connections – the degree to which two sets of numbers (called variables) are associated with each other – and it can also clarify the relationship between them.

Insightful correlations are plentiful for legal managers if they collect the data. Consider law firms working with a law department: a general counsel might suspect a connection between their overall effective billing rate and their number of lawyers. Or perhaps a lawyer’s gut feeling is that the more years practicing law an in-house counsel has, in general, the less closely she or he manages their outside counsel spend. A billing partner might suspect that the longer an invoice goes unpaid, the lower the realization rate. After collecting some data, someone can run a correlation and test those suppositions.

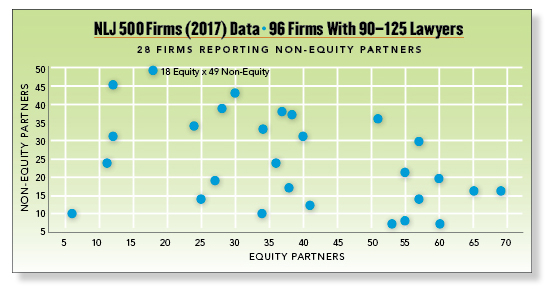

To explain correlation with real data, let’s hypothesize that the more equity partners a law firm has, the more non-equity partners it is likely to have. We can find out by using data from the NLJ 500 list (ALM). To have a more homogenous set, we focus on the 96 law firms that reported between 90 and 125 lawyers, where it turns out that only a third of them (28 firms) reported non-equity partners.

Before figuring out the correlation that will answer our hypothesis, sound statistical practice says to plot the data. Our eyes easily spot oddities in the data and even patterns. We particularly want to avoid wasting time on correlations where the variables are not linearly related to each (such as if they include squares or cubes). Correlation is an appropriate numerical measure only for linear relationships, and is sensitive to outliers (values at the extremes).

In the plot, the horizontal, x axis tells how many equity partners each of the 28 firms reported, while the y axis tells the firm’s number of non-equity partners. For example, the highest number of non-equity partners was 49 at a firm with 18 equity partners. (We could have added a best-fit regression line, but that’s for another column.)

At a glance you can see that this scatter plot suggests no outliers and displays a linear relationship between the two variables. So we can proceed and calculate the correlation coefficient, which measures the strength and direction of a linear relationship between two quantitative variables. For the 28 law firms, the correlation between the number of equity and non-equity partners is -0.41, a moderately strong NEGATIVE correlation. Our hypothesis was wrong: actually, as law firms of this size have more equity partners, they tend to have fewer non-equity partners.

Correlation coefficients always range between -1 and 1. Values near -1 indicate a strong negative linear relationship (as is our negative 0.41 value), values near 0 indicate a weak linear relationship, and values near 1 indicate a strong, positive linear relationship. A negative correlation means that one variable is less likely to be below the average of that variable when the other variable is below its average.

Let’s extend our understanding of correlation with some additional observations.

- Correlation disregards the units of measurement of the variables. Inches can correlate to dollars, or speed with age. The correlation coefficient can be computed and interpreted for any two numeric variables.

- Because all correlations range between -1 and 1, you can compare correlations between different pairs of variables. So, we might find and say that there is a stronger correlation between the number of equity partners and the number of associates.

- We can calculate correlations between ratios, such as between R&D spending as a percentage of revenue and patent lawyers as a percentage of all the lawyers in a law department.

- If certain assumptions are met, we can interpret the confidence interval of the correlation coefficient (what range the coefficient would likely fall in if we redid the calculation on lots of samples from the data) and test the null hypothesis, that there really is no correlation between the two variables (and any correlation you observed is a consequence of random sampling).

- If both variables are normally distributed (think bell curve), the proper method is the Pearson coefficient [the covariance (see below) of the two variables divided by the product of their standard deviations]. Another method, Spearman’s rank correlation, does not assume that the underlying data is distributed in a statistically normal way.

- Usually there is an intuitive explanation for a strong positive or negative correlation. With our scenario, firms that believe in full ownership and equity participation of their partners are probably less likely to create a tier of non-equity partners.

- Correlation differs from regression. Correlation is not predictive. That is, correlation can only tell us how closely one set of numbers is associated with another set. By contrast, regression enables us to predict one variable based on another.

Simply to know the direction and strength of the relationship between two metrics gives legal managers useful insights. But even if no significant correlation exists between two metrics, that finding too can help managers. For example, what if it turns out that there is no statistically meaningful correlation between the average number of lawyers in a law department per office location and total legal spending? That realization might suggest that it doesn’t much matter about the number of in-house lawyers at various locations. We should point out, however, that a lack of correlation does not necessarily imply a lack of relationship; the variables could have a non-linear (e.g., curved, step or bimodal) relationship. Using our data set, the correlation turns out not to be statistically significant, meaning that it could be a function of chance.

Always remember that correlation does not prove causation. Just because the degree of regulation of an industry correlates with higher legal spend per billion of revenue does not mean that regulation is the CAUSE of those legal expenses (nor do bulging legal bills cause regulations!). Other factors may be at work such as political influence, case-law development, maturity of the industry, or specific legislation. Sometimes a third factor accounts for the close relationship between one metric and another, such as concentration in an industry. Statisticians refer to those behind-the-scenes factors as lurking variables.

One way to remove the effect of a possible lurking variable from the correlation of two other variables is to calculate a partial correlation. A partial correlation is the correlation that remains between two variables after removing the correlation that is due to their mutual association with one or more other variables. By looking at a graphic of the partial correlation coefficient matrix among the variables (like a heat map), it may be visually clear that the partial correlation between some of them is quite high.

Let’s add one more math concept related to correlation. Covariance tells how much two sets of variables vary together. It’s similar to variance, but where variance tells about a single variable’s distribution, covariance tells you how two variables vary together. The larger the values of the variables, the larger the covariance. For our data set of 28 law firms, the covariance of equity partners and non-equity partners is -91.8. If we divide that covariance by the product of both variables’ standard deviations we arrive at the correlation coefficient given above.

We emerge from this brief dive into mathematical methods. The key takeaway from this column is that correlation tools stand ready to help managers of lawyers to more crisply understand data variables that might vary together. Managers need not rely only on their own experiential sense of two sets of numbers changing in relation to each other. Correlation can put precision to intuitive insights and can clarify the direction of the variation and its credibility.